Your Local Mortgage Lender

Located in Edina, Minnesota

Personalized Mortgage Experience

Alex Mysinek offers personalized service and loan options you'll love. We shop multiple lenders to find the best rate and product for you, getting you into your dream home faster.

With wholesale interest rates and cutting-edge technology, we make the mortgage process seamless. Trust the experts who focus solely on mortgages. Support your local community and experience elite client service.

Let us help you achieve your homeownership dreams!

The Home Loan Process

Mortgage Pre-Approval

Get pre-approved from one of our Loan Officers to see how much you can afford.

House Shopping

Work with a trusted Real Estate Agent to find a home you would like to move into.

Loan Application

Complete your home loan application to get the lending process started.

Don't take my word for it

Mortgage Programs

Experience the best mortgage experience located in Edina, Minnesota.

Home Loan Options

Our experienced mortgage advisors will walk you through the best mortgage loan program that will fit your specific scenario.

Conventional Home Loans.

FHA Home Loans.

USDA Home Loans.

VA Home Loans.

Frequently Asked Questions

How often can I refinance my mortgage?

There is no limit to the number of times you can refinance. However, you must qualify every time you apply and there will be costs associated with closing the loan each time.

Can I buy a home if I do not have money for a down payment?

Yes! There are a number of bond programs that offer low or no down payment financing options.

How do I know which mortgage is right for me?

The key to choosing the right mortgage is to understand the range of options and features available to you, as well as your budget, circumstances, and goals. Our licensed mortgage professionals are here to help you navigate that process. The more you know, the more comfortable and confident you will be choosing the best option for you and your family.

How long will the loan process take?

The Truth in Lending Act (TILA) does not permit a lender to close a loan until at least seven (7) business days have passed from the date your application was received. A typical home loan takes 30 days, as a number of third-party services such as appraisals, title work, and credit are required in conjunction with the mortgage process. Once you familiarize your Loan Officer with the details of your specific loan scenario, they will be able to provide you with a more specific timeline.

Will I qualify for a home loan?

The only way to find out is to speak with a qualified mortgage professional. Our Loan Officers have helped numerous clients who didn’t know if they could qualify to become home owners. We take the time to understand your financial situation and long-term financial goals, and then match you with the loan program that best fits your needs. Your approval for a loan may also largely depend on the price of the home you are financing. Getting pre-qualified prior to beginning your home search can give you an idea of what you may be able to afford.

Why do people refinance their mortgages?

Homeowners typically refinance to save money, either by obtaining a lower interest rate or by reducing the term of their loan. Refinancing is also a way to convert an adjustable loan to a fixed loan or to consolidate debts.

How much money will I have to pay upfront to buy a home?

This question does not have a simple, one-size-fits-all answer. The exact amount will depend on the price of the home you buy as well the type of mortgage financing you choose. Depending on your loan program, your down payment could be as much as 20% of the home’s price or as little as 3%, while some loans require no down payment at all.

Can I get a mortgage after bankruptcy?

You may still qualify for a home loan even if you have experienced a bankruptcy. The best way to find out if you qualify is to talk with a Loan Officer to discuss your options. Be sure to bring all paperwork regarding your bankruptcy so your Loan Officer can find the program that best fits your situation.

Should I lock my interest rate now, or wait until we are closer to our closing?

Interest rates fluctuate all day, every day. If an interest rate is good, it may be in your best interest to lock now. If you wait, you run the risk of an increase in rates later. If you are concerned that rates may go down after you lock, contact your Loan Officer to discuss your options. Some programs allow you to lock for an extended period and choose to lower your rate should a better one become available.

Most Recent Blog Updates

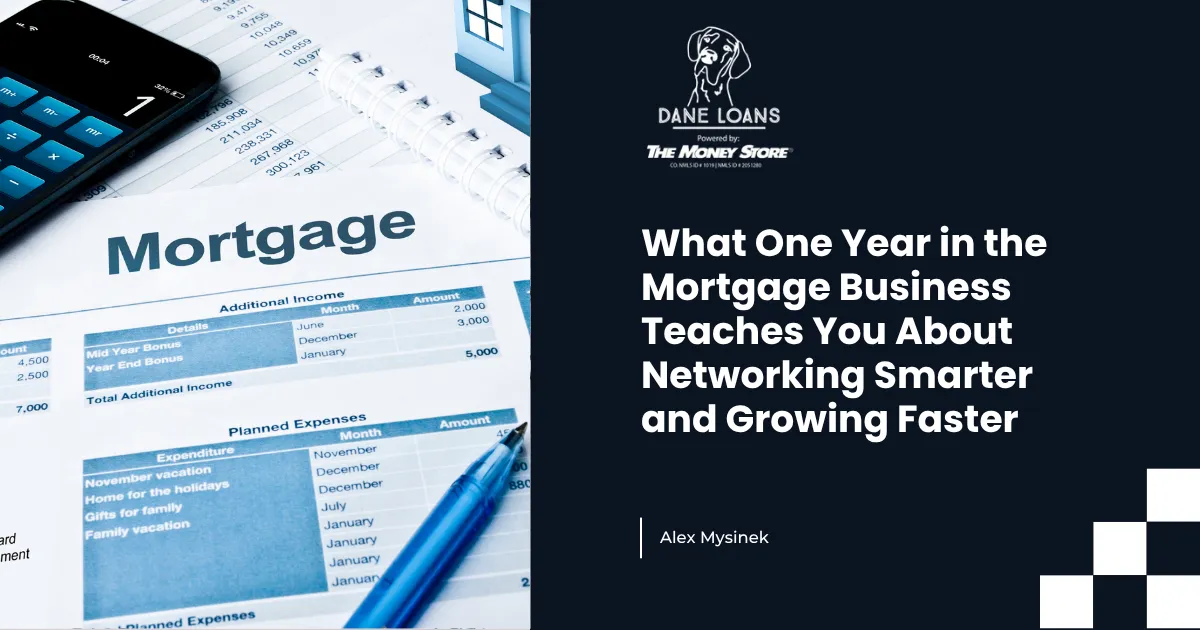

What One Year in the Mortgage Business Teaches You About Networking Smarter and Growing Faster

What One Year in the Mortgage Business Teaches You About Networking Smarter and Growing Faster

The Lesson Most New Loan Officers Learn the Hard Way

The first year in the mortgage business teaches you a lot. Some of it confirms what you expected. Most of it surprises you. And the lessons that stick hardest are usually the ones about where your time actually produces results versus where it feels productive but does not move the needle.

After a full year of figuring out what works and what does not Alex Mysinek has a clear picture of where the next two to three years need to go and the strategy looks meaningfully different from what year one looked like.

Why Big Networking Events Are Not the Answer

Large networking events have an appealing logic. A room full of professionals, potential referral partners, and new connections all in one place. The efficiency argument seems sound on the surface. More people, more potential opportunities, more chances to get your name out there.

The reality in practice is different. Big events produce surface-level connections that rarely convert into actual business relationships. The conversations are brief, the follow-up is inconsistent, and the return on the time invested is difficult to justify when you honestly evaluate what actually came from those evenings.

The shift that changes the outcome is moving from volume-based networking to depth-based networking. Lunches and coffees with specific people, intentional one-on-one conversations that build actual relationships rather than exchanging business cards in a crowded room. The number of interactions goes down. The quality and the conversion rate go up.

What Niche Networking Actually Means

Niche networking is not just about smaller gatherings. It is about being deliberate about who you are spending time with and why. For a loan officer that means identifying the specific referral partners, real estate agents, financial advisors, and professional contacts who serve the same clients you want to work with and investing in those relationships specifically.

A lunch with one well-connected real estate agent who genuinely understands your value proposition is worth more than an evening at an event with fifty people who barely remember your name the next day. The math works differently when the relationships are deeper and more targeted.

Cold Calling and Coaching Up the Team

The other major focus for the next phase of growth is locking into cold calling more consistently and getting cold callers coached up on how to convert warm and nurtured leads rather than just generating initial contact.

The difference between a cold caller who can identify and nurture a warm lead and one who simply moves through a list is the difference between a pipeline that builds over time and one that requires constant replacement. Teaching the team how to recognize where a prospect is in their decision process and how to maintain contact at the right cadence is the skill that turns outreach activity into closed transactions months down the road.

Why CRM Consistency Is the Foundation

Everything else in a growth strategy depends on staying consistently in touch with the right people at the right time. A CRM that is actively maintained with clear stage designations, warm, hot, cold, and a follow-up cadence that reflects where each contact actually is in the process is what keeps opportunities from falling through the cracks.

As Alex Mysinek explains you never know when someone is ready to transact. The person who was not ready six months ago may be ready today. The key is staying in touch in a reasonable and consistent way without wasting time on contacts who are genuinely not moving. A well-maintained CRM makes that distinction visible and keeps the follow-up targeted rather than scattered.

The loan officers who build sustainable businesses are not the ones who work the hardest in any given week. They are the ones who stay consistently present with their network over months and years in a way that means their name is the first one that comes to mind when someone is ready to move.

Alex Mysinek works with buyers and referral partners who are ready to have a real conversation about financing. Reach out to Alex Mysinek to connect directly.

Sources

MortgageNewsDaily.com HousingWire.com NationalMortgageProfessional.com Entrepreneur.com Forbes.com

Mortgage Calculator

See your total mortgage payments using the tool below.

| Year | Interest | Principal | Balance |

|---|

Social Media Links

YouTube